Economic outlook: Waiting on recession

Since our October Cyclical Outlook, “Prevailing Under Pressure,” economic activity has been more resilient than expected, while inflation has remained elevated. However, the outlook – as measured by surveys of business leaders and purchasing managers – has deteriorated, as banks have tightened credit conditions, industrial order books have waned, and consumers have depleted elevated savings. Financial conditions also remain tight as central banks raised market expectations for the level of policy rates, while crystalizing what’s priced in with actual hikes.

As a result, some kind of recession over the next 12 months still appears likely across developed markets (DM). Unlike other modern recessions, where rate hikes in anticipation of inflation triggered broader market stress, this recession and rising unemployment could be the cost of returning inflation to target levels. Our baseline view is that recessions in 2023 will be modest, although we are preparing for a range of possible outcomes.

We would emphasize three themes heading into 2023:

1) Inflation is likely to moderate, and risks to the inflation outlook appear more balanced.

Supply constraints, related first to the pandemic and later to the war in Ukraine, together with a stimulus-induced demand surge and an acceleration in unit labor costs, have all added to inflation. However, now that most price adjustments appear to be behind us, some of this inflation is likely to fade away with little central bank help.

For example, the 40% and 50% increase in U.S. used car and global energy prices, respectively, contributed 4 percentage points to U.S. headline inflation in 2022. If those prices just stabilize, U.S. headline consumer price index (CPI) inflation could fall from about 8% to 4% (annualized) relatively quickly, in our view.

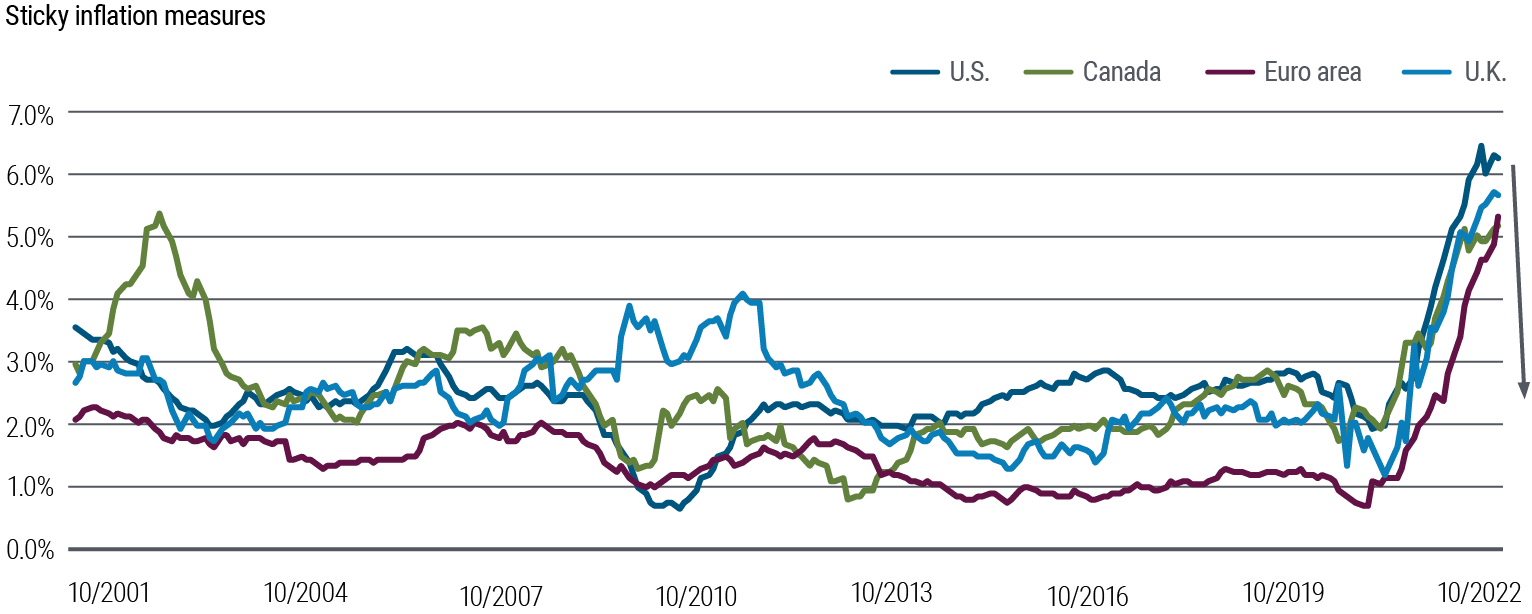

Going from 4% to 2% would take more time, as the “stickier” categories may be slow to moderate (see Figure 1). Tight labor markets across DM have elevated wage and unit labor cost inflation. Shelter and rental inflation are expected to only gradually moderate.

Figure 1: Sticky inflation measures close to peaking

The faster-than-expected economic reopening in China could quicken the easing of supply-chain disruptions. We believe consumption, especially in services, will drive that reopening, limiting any pressure on global goods inflation.

2) Central banks are closer to holding policy at restrictive levels as opposed to getting policy to restrictive levels.

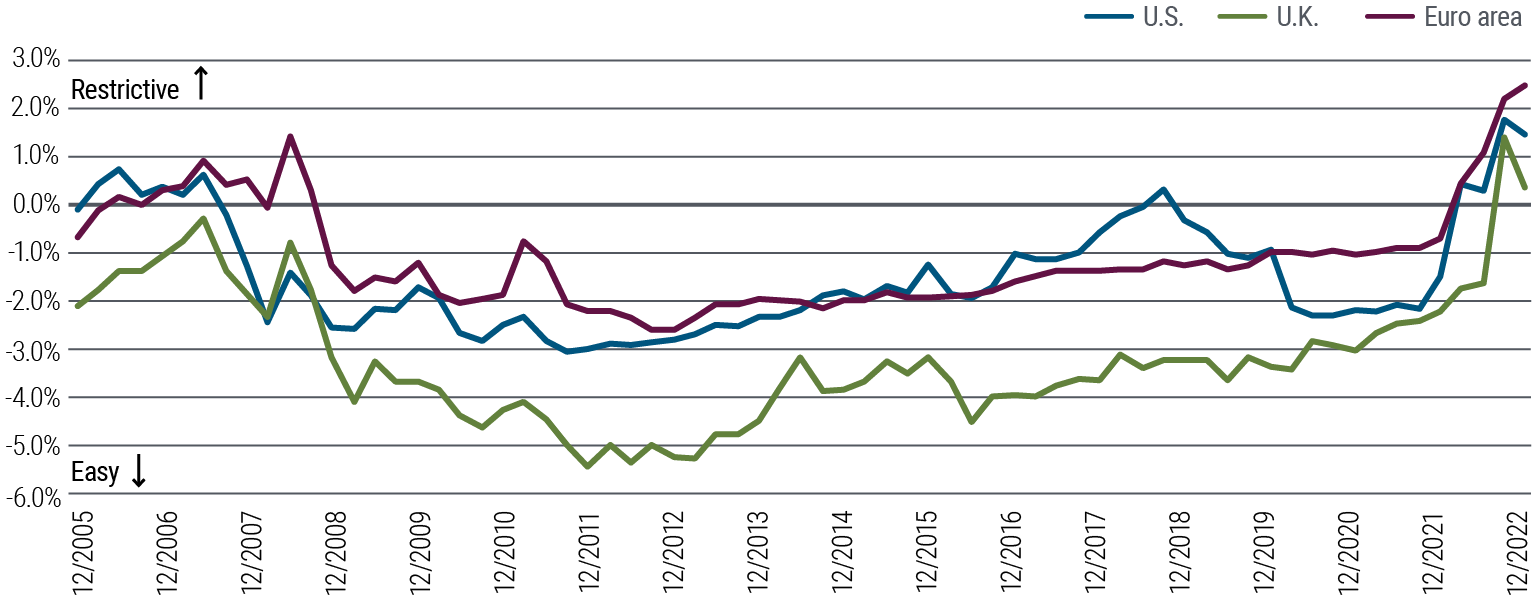

Monetary policy has likely already reached restrictive levels in several major economies – see Figure 2. While nominal DM overnight rates are still below inflation, that is likely to change as inflation moderates and central banks reach points where they pause their hiking cycles.

Figure 2: Monetary policy already appears to be restrictive in several developed markets

We think the U.S. Federal Reserve (Fed) may need to reach a roughly 5% nominal federal funds rate, which is already largely priced into markets and reflected in the Fed’s own projections. (For more, see our recent Viewpoint, “Don’t Fight the Fed, But Don’t Lose the Thread.”)

Estimates put the real neutral interest rate in Europe well below other DM rates, suggesting the European Central Bank (ECB) has less work to do. We think a 3% rate, or slightly higher, where the ECB pauses is a reasonable estimate, given the euro area is likely close to if not already in a recession, and that inflation may peak in the fourth quarter of 2022 or early 2023. (For more, see our recent blog post, “ECB Hikes, and Indicates Higher Rates Coming.”)

The Bank of England and Bank of Canada are likely targeting nominal rates somewhere between the ECB and the Fed. Estimates of their real neutral rates are above that in Europe.

Overall, DM central banks have already largely realigned market pricing with the need for restrictive policy and have achieved this relatively quickly, with little additional market stress or contagion. The pace of tightening according to our financial conditions index (which includes rates, equity, credit, and foreign exchange) has mirrored that during the 2008 global financial crisis, with little deterioration in market functioning and without a sudden stop in credit markets, which could result in a more severe economic outcome.

Developed market central banks have largely realigned market pricing with the need for restrictive policy.

While we expect DM central banks to continue to hike for the next quarter or so, before holding policy in restrictive territory, the trade-off they face will eventually change. Today, with low unemployment and elevated inflation, restrictive policy is needed. As 2023 progresses, inflation moderates, and unemployment rises, the need for restrictive policy will get less clear.

Since the U.S. appears to be leading DM inflationary trends, and inflation could fall faster in the U.S. than elsewhere, the Fed may be the first central bank to discuss cutting rates in the second half of 2023.

3) Shallow recessions won’t be completely painless.

As tighter financial conditions cool inflation over time (monetary policy works through lags), the mechanism won’t be painless for the real economy, since it largely works through weakening the labor market.

Using data spanning back to the 1960s across 14 developed markets, we estimate the increase in unemployment needed to moderate inflation. We find central banks could need to increase the unemployment rate by around 0.7 percentage points to bring inflation down by 1 percentage point. By that measure, U.S. unemployment may have to increase to around 5%, from 3.5% in December, to moderate the sticky inflation over time.

The U.S. labor market is one of the tightest across DM, and consequentially unit labor cost inflation is well above both DM peers and levels consistent with the Fed’s 2% long-term inflation goal. Similar measures in other regions are also elevated. In the European Union and U.K., unit labor cost inflation is running around 4% year-over-year, while Canada’s is slightly higher. Unemployment likely will need to rise across these regions as well.

Bottom line: Recession likely, but soft landing plausible

The U.K., which is likely already in a recession, appears to be leading the DM downturn. We expect the euro area to follow, and the U.S. and Canada to slip into recession later in the first half of 2023. Euro area and U.K. inflation appear to be following the U.S. with a lag. We expect euro area and U.K. headline inflation to peak just above 10% in the fourth quarter of 2022, while U.S. CPI inflation likely peaked near 9% in mid-2022.

Japan stands out as relatively more resilient, with expected growth at or slightly above trend, as the relaxation of economic restrictions helps offset global headwinds. Core rates of Japanese inflation have firmed, increasing the likelihood that the Bank of Japan further alters its yield curve control framework, following the first adjustment announced in late December after our Cyclical Forum.

Fiscal policy is likely to be muted, despite economic weakness, with much less impact on the 2023 outlook in the U.S. and Canada. Fiscal support packages in Europe and the U.K. to offset higher energy costs aren’t likely enough to stave off recession.

Fiscal policy is likely to be muted, despite economic weakness, with much less impact on the 2023 outlook in the U.S. and Canada.

Macro uncertainty is still high and there are risks. Linkages between real economies and global markets, coupled with the fastest pace of financial conditions tightening in decades, elevate the risk of accidents, contagion, and credit market disruption.

Yet there is still a plausible path to a soft landing as labor hoarding amid still-scarce supply, as well as moderating inflation, reaccelerate real income growth. Consumer and business balance sheets are strong, with elevated cash reserves, while pandemic-related supply constraints created large order backlogs, pent-up demand, and margin expansion, which are all likely to support business activity. China’s reopening may also provide a tailwind to the global economy.